Demand Has Arrived. Infrastructure Has Not.

For months, the digital asset industry has celebrated the rapid growth of tokenized stocks.

Demand for blockchain-native securities has arrived. Market infrastructure has not.

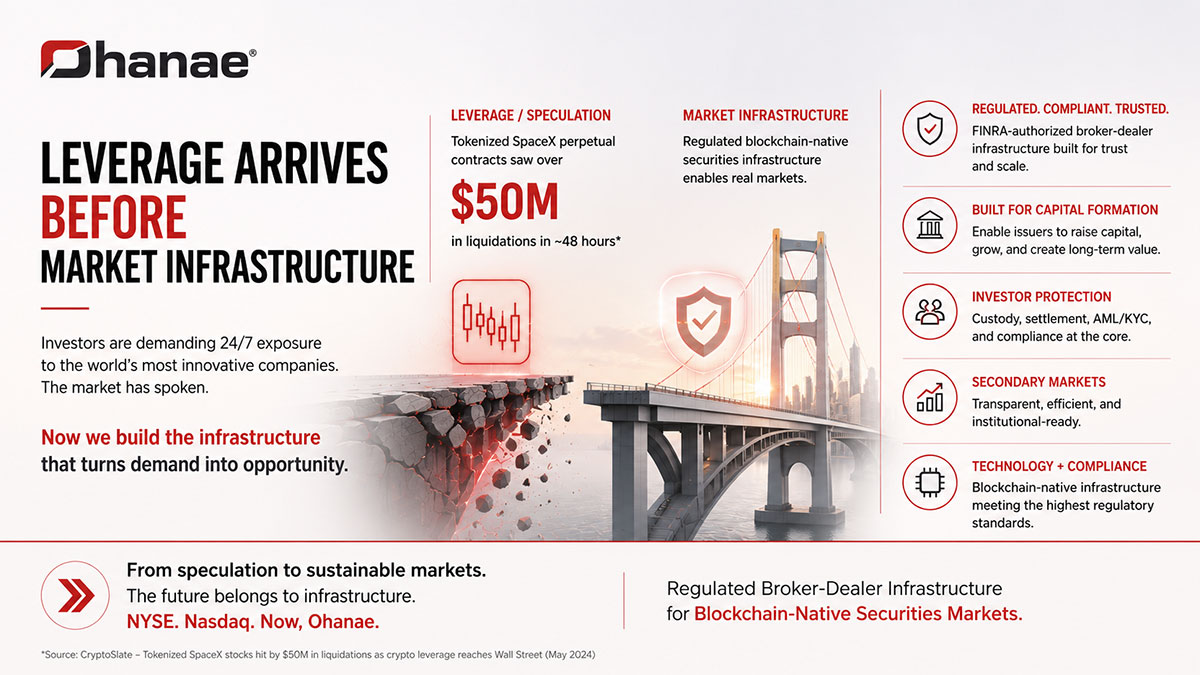

The recent $50 million liquidation of tokenized SpaceX perpetual contracts illustrates a fundamental shift in capital markets. Investors clearly want 24×7 access to private-company exposure. The missing piece is the regulated infrastructure capable of supporting that demand.

Pantera May Have Identified the Bigger Opportunity

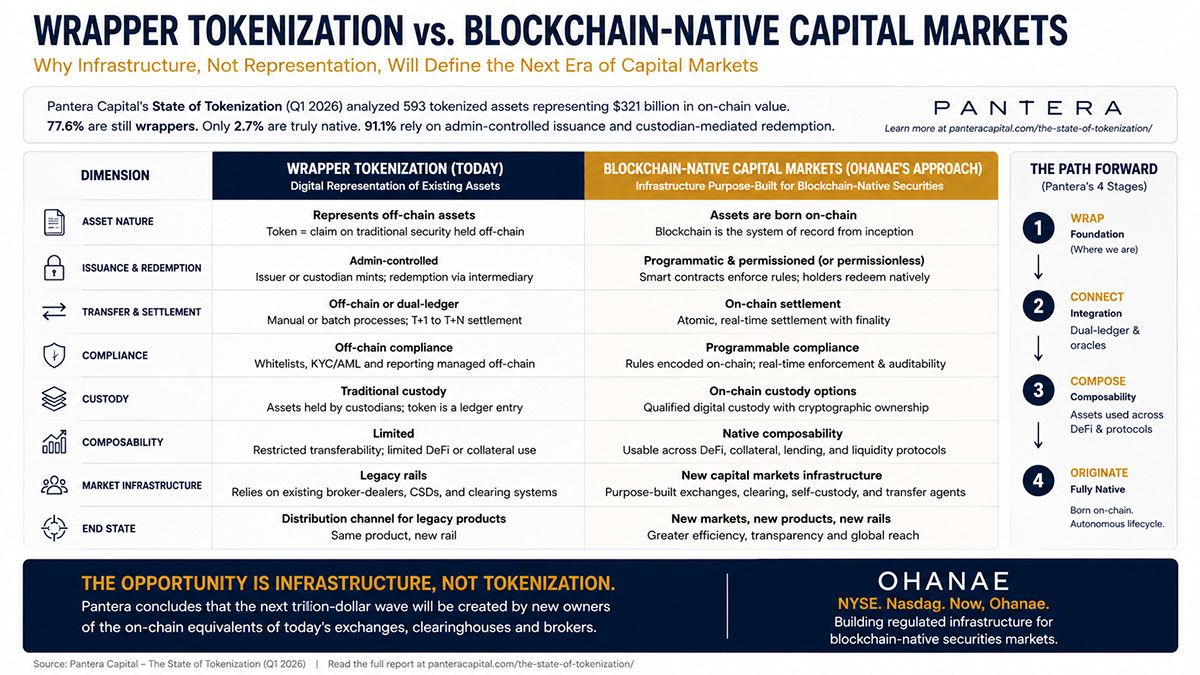

Earlier this month, Pantera Capital published one of the most comprehensive studies of the tokenization industry.

Its conclusion was striking.

Of nearly 600 tokenized assets representing over $321 billion, approximately:

- 77.6% remain wrappers of traditional assets.

- Only 2.7% are truly blockchain-native.

- Most still depend on traditional custodians and off-chain infrastructure.

Pantera's conclusion was simple:

The opportunity is infrastructure—not tokenization.

CryptoSlate's report provides real-world evidence supporting Pantera's conclusion. Investor demand is accelerating, yet much of today's market still relies on wrappers and synthetic instruments rather than blockchain-native securities.

The recent SpaceX liquidation event illustrates precisely why the market's next phase will be defined not by who creates the next tokenized product, but by who builds the regulated infrastructure capable of supporting blockchain-native capital markets.

What Actually Happened?

The SpaceX products generating these liquidations were not ownership interests in SpaceX.

Instead, they were leveraged perpetual contracts whose prices referenced SpaceX's valuation.

They provide price exposure—but not ownership.

Investors do not receive:

- Equity ownership

- Shareholder rights

- Voting rights

- Capital formation for the issuer

- Transfer agent services

- Regulated custody

- Regulated clearing and settlement

They create trading activity.

They do not create capital markets.

The Most Important Point Is Who Cannot Participate

Equally important is who these products are unavailable to.

Today's wrapper and synthetic tokenized stock products offered by many global crypto exchanges are generally not available to U.S. persons because of U.S. securities laws and regulatory requirements.

As a result, despite significant international interest, these products remain largely inaccessible to the world's largest capital market.

That point should not be overlooked.

The first generation of tokenized stock products has focused primarily on creating offshore trading exposure—not on building regulated securities market infrastructure capable of serving U.S. issuers and investors.

Demand Is No Longer the Question

For years, many questioned whether investors actually wanted blockchain-based securities.

I believe that question has now been answered.

Investors clearly want:

- 24×7 markets

- Faster settlement

- Global accessibility

- Blockchain-native ownership

- Access to private company investments

The challenge is no longer proving demand.

The challenge is building the regulated infrastructure capable of supporting that demand.

Throughout the history of financial markets, lasting enterprise value has been created not only by financial products, but by the trusted infrastructure that enables those products to scale.

From stock exchanges and clearing houses to custodians and transfer agents, enduring value has historically accrued to the institutions that make markets possible—not simply to the products traded on them.

Capital Formation vs. Speculation

Speculative trading products generate trading volume.

They do not finance companies.

Real capital markets help entrepreneurs build businesses.

They connect issuers with investors.

They support long-term economic growth.

That is a fundamentally different mission.

From Tokenization to Market Structure

For years, the industry has focused on tokenization.

At Ohanae, we have focused on market structure.

We believe blockchain's greatest opportunity is not simply representing existing securities as digital tokens.

It is building the next generation of regulated market infrastructure that enables issuers to raise capital, investors to participate with confidence, and securities to trade seamlessly in blockchain-native markets.

Pantera's research suggests the next wave of value creation will belong to infrastructure rather than wrappers.

CryptoSlate's latest article demonstrates that investor demand is already here.

Demand has already arrived.

Infrastructure is next.

That is where the next generation of capital markets will be built.

NYSE. Nasdaq. Now, Ohanae.

Regulated Broker-Dealer Infrastructure for Blockchain-Native Securities Markets.

Further Reading

Pantera Capital

State of Tokenization (Q1 2026)

CryptoSlate

Tokenized SpaceX Stocks Hit by $50M in Liquidations as Crypto Leverage Reaches Wall Street